The interaction of time- and country-fixed effects eg. Controlling for variables that are constant across entities but vary over time can be done by including time fixed effects.

Fixed Effects Regression Results Specifications With Relative Download Table

Country-year fixed effects is used to control for country level loan demand and other time varying country level effects omitted variables.

. First I xtset my data and then I run a regression. X kit represents independent. Your best case scenario is you have a lot of firms and a long panel per firm 8.

Unfortunately this terminology is the cause of much confusion. I have a panel of annual data for different firms over several years of time. It also can depend on your data structure.

The other thing with fixed effects estimation in Stata is that many people are deceived by the xtset command where you can set a panel and a time variable. EViews Gareth EViews Moderator. Dummy A equals to 1 for firm A 2010 2011 and 2012.

I would like to run the following fixed effects for industryyear regression code. Xtset Firm Year xtreg DepVar Var1 Var2 Var3 iYear fe. If you have a simple regression of yon x then adding the industry and year fixed effects is as simple as.

30 Jun 2017 0739. The problem is that the outcome seems to be taking into. For technical questions regarding estimation of single equations systems VARs Factor analysis and State Space Models in EViews.

However I do need to control for firm fixed effect for each individual firm presumably by adding a dummy variable for each firm - eg. If you believe that these unobservable factors are time-invariant then fixed effects. The term fixed effects model is usually contrasted with random effects model.

Fixed effects You could add time effects to the entity effects model to have a time and entity fixed effects regression model. Fixed Effects- Industry and Year. 1 is under firms control but x 2 is not.

And then for years 2013-2018 the firms patent portfolio would equal 1. This fixed-effects specification absorbs factors such as the demand for bank debt in a particular country at a particular time. We can use the fixed-effect model to avoid omitted variable bias.

Firms fixed effect - it is a firm specific dummy that will tell you what unique effect firm specific and time invariant unobservables are having on the regressand. It is still not clear. In time may affect a predictor variable at a later point in time.

If there are only time fixed effects the fixed effects regression model becomes Y it β0 β1Xit δ2B2tδT BT t uit Y i t β 0 β 1 X i t δ 2 B 2 t δ T B T t u i t where only T 1 T 1 dummies are included B1 B 1 is omitted since the model. Also called longitudinal data are for multiple entities eg geo-location states across multiple time periods eg year or month. Fixed effects model in STATA This video explains the concept of fixed effects model then shows how to estimate a fixed effect model in STATA with complete.

It is the key ingredient for fixed effect regression. In the classic view a fixed effects model treats unobserved differences between. Regress y x iindustry iyear.

If the set of firms in an industry never changes there is again a multicollinearity violation as the sum of all dummy variables for firms in an industry is equal to the sum of all dummy variables for the industry. Industry fixed effect - as above but this tell you the effect of industry specific and time invariant unobservables on the regressand. Hi Steve Sorry for the misunderstanding.

Y it β 0 β 1X 1it β kX kit γ 2E 2 γ nE n δ 2T 2 δ tT t u it eq3 Where Y it is the dependent variable DV where i entity and t time. Until the year 2013. The other fixed effects need to be estimated directly which can cause computational problems.

I just need to run one regression for the entire panel. My sample includes 31800 firms from 2004-2017. Check the examples here to see how your data should be formatted for panel data modeling.

The year dummies will pick up any variation in the outcome that happen over time and that is not attributed to your other explanatory variables. Firm fixed and time fixed effects. In your quaterly data it will be difficult to compute a year fixed effect models without aggregating your data to make them yearly.

Think of fixed effects as adding dummies for each time period time fixed effects and for each id firm fixed effects. To highlight the previous point firm CN9360002267 acquired patent_id CN101618297A in year 2013. I want to include firm and year fixed effects.

Note how including year FE reduces P variation but not T which indicates that most of the T variation comes from spatial differences whereas a lot of the P variation comes from year-to-year. If my display policy doesnt change the. Only the panel variable is used to.

For example to estimate a regression on Compustat data spanning 1970-2008 with both firm and 4-digit SIC industry-year fixed effects Statas XTREG command requires nearly 40. Including firm and industryyear fixed effects means including a dummy variable for all firms and also a dummy variable for all industry-year combinations. CEObackground MBACEO and FemaleCEO are time-invariant dummies for each CEO and industry time-invariant dummy for firm while rest are time varying firmCEO attributes.

I want to run firm year fixed effect regression. If x 1 is price x 2 is promotion like a display. Firms fixed effects and industry year fixed effect - this was already covered in.

Using unit fixed effects which are probably firms when you only have a few firms and lots of years of observations versus when you have a lot of firms and only a few years of observations each create different problems. General econometric questions and advice should go in the Econometric Discussions forum. The different rows here correspond to the raw data no fixed effect after removing year fixed effects FE year state FE and year district FE.

A Cross-sectionTime Series Location Year Price Per capita Quantity Chicago 2003 75 20 Chicago 2004 85 18 Peoria 2003 50 10 Peoria 2004 48 11 Milwaukee 2003 60 15. If we use our data to estimate the relationship between x 1 and x 2 then this is the same using OLS from y on x 1. Here is oneway to do that.

Suppose both variables are under firms control. If you plug in all time dummies leave out one year of course in your FE estimation you will have both fixed time and firm effects. Its not problematic and is even a good idea.

Dear all I have a panel dataset of 250 firms over the period 1996-2016. Year id summarize y mean y x mean x. Thus ideally I would like to have a year variable for firm CN9360002267 that takes a value of 0 for year 2000 0 for year 2001 and so on.

Require plyr yeardata.

Should We Include The Industry Variables When We Control For Year Industry Fixed Effects R Econometrics

Firm Fixed Effects And Year Dummies Firm Clustered Standard Errors Download Scientific Diagram

18 Regression Results Of Fixed Effect Firm And Time Model Download Scientific Diagram

What Is The Difference Between Region Year And Region Year Fixed Effects

What Does Firm Time Fixed Effect Says Why Is It Chegg Com

The Importance Of Year Fixed Effect And Robust Standard Error

Results Of Fixed Effects Estimator With Time Dummies Download Scientific Diagram

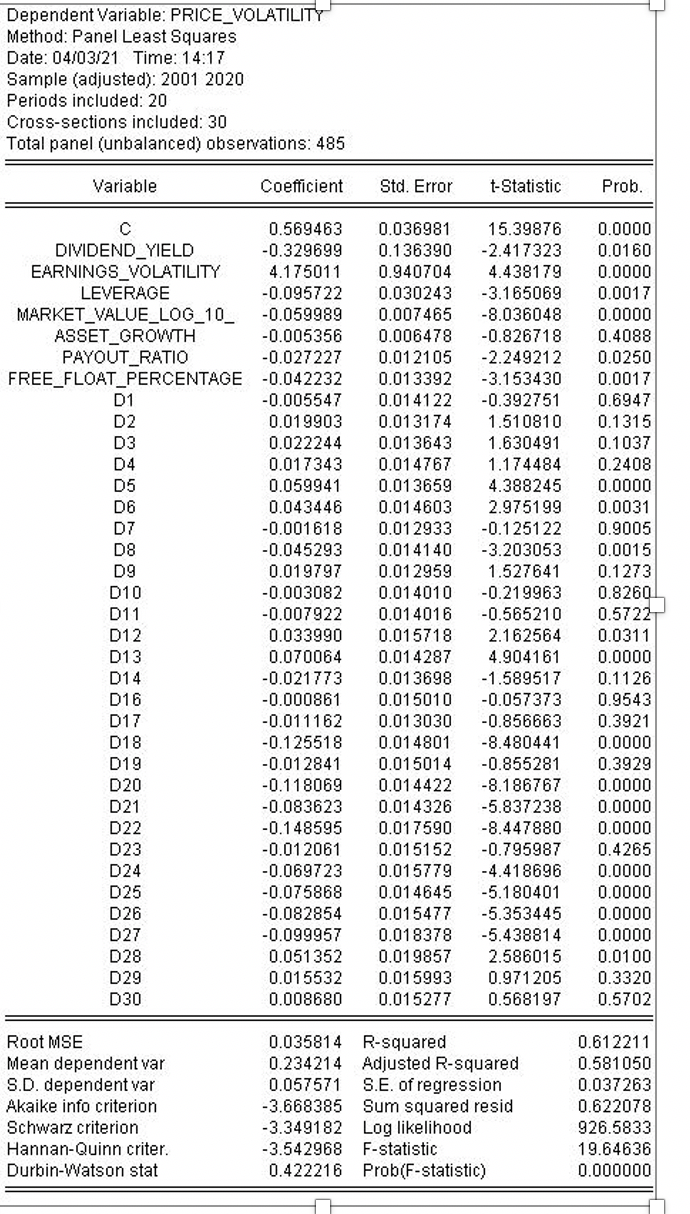

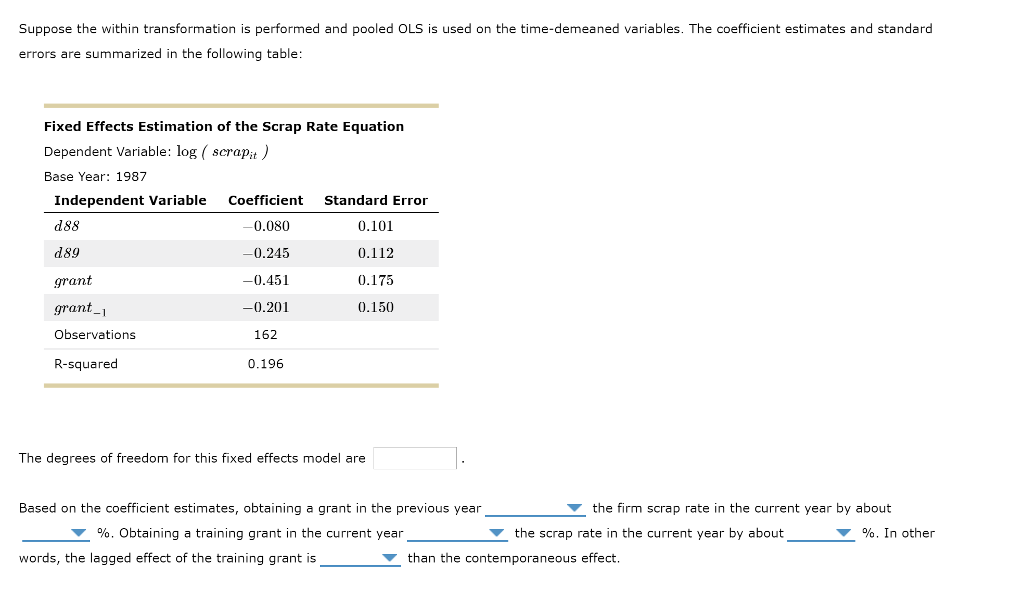

14 Interpreting Fixed Effects Estimation Suppose A Chegg Com

0 comments

Post a Comment